毫升 |信用卡欺诈检测

挑战在于识别欺诈性信用卡交易,以便信用卡公司的客户不会因为他们没有购买的商品而被收取费用。

信用卡欺诈检测涉及的主要挑战是:

- 每天都会处理海量数据,模型构建必须足够快才能及时响应骗局。

- 不平衡数据,即大多数交易(99.8%)不是欺诈性的,这使得检测欺诈性交易变得非常困难

- 数据可用性,因为数据大多是私有的。

- 错误分类的数据可能是另一个主要问题,因为并非每笔欺诈交易都会被捕获和报告。

- 诈骗者对模型使用的自适应技术。

如何应对这些挑战?

- 所使用的模型必须足够简单和快速,以检测异常并将其尽快归类为欺诈交易。

- 不平衡可以通过适当使用一些我们将在下一段中讨论的方法来处理

- 为了保护用户的隐私,可以减少数据的维数。

- 必须采用更可靠的来源来仔细检查数据,至少在训练模型时。

- 我们可以使模型简单且可解释,这样当诈骗者通过一些调整来适应它时,我们就可以启动并运行一个新模型来部署。

在进入代码之前,需要在 jupyter notebook 上工作。如果您的机器上没有安装,您可以使用 Google colab。

您可以从此链接下载数据集

如果链接不起作用,请转到此链接并登录 kaggle 下载数据集。

代码:导入所有必要的库

# import the necessary packages

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from matplotlib import gridspec

代码:加载数据

# Load the dataset from the csv file using pandas

# best way is to mount the drive on colab and

# copy the path for the csv file

data = pd.read_csv("credit.csv")

代码:理解数据

# Grab a peek at the data

data.head()

代码:描述数据

# Print the shape of the data

# data = data.sample(frac = 0.1, random_state = 48)

print(data.shape)

print(data.describe())

输出 :

(284807, 31)

Time V1 ... Amount Class

count 284807.000000 2.848070e+05 ... 284807.000000 284807.000000

mean 94813.859575 3.919560e-15 ... 88.349619 0.001727

std 47488.145955 1.958696e+00 ... 250.120109 0.041527

min 0.000000 -5.640751e+01 ... 0.000000 0.000000

25% 54201.500000 -9.203734e-01 ... 5.600000 0.000000

50% 84692.000000 1.810880e-02 ... 22.000000 0.000000

75% 139320.500000 1.315642e+00 ... 77.165000 0.000000

max 172792.000000 2.454930e+00 ... 25691.160000 1.000000

[8 rows x 31 columns]

代码:数据不平衡

是时候解释我们正在处理的数据了。

# Determine number of fraud cases in dataset

fraud = data[data['Class'] == 1]

valid = data[data['Class'] == 0]

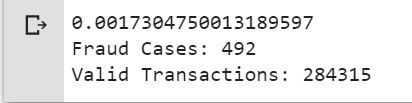

outlierFraction = len(fraud)/float(len(valid))

print(outlierFraction)

print('Fraud Cases: {}'.format(len(data[data['Class'] == 1])))

print('Valid Transactions: {}'.format(len(data[data['Class'] == 0])))

所有交易中只有0.17%的欺诈交易。数据高度不平衡。让我们首先应用我们的模型而不平衡它,如果我们没有得到很好的准确性,那么我们可以找到一种方法来平衡这个数据集。但首先,让我们在没有它的情况下实现模型,并且仅在需要时才平衡数据。

代码:打印欺诈交易的金额详细信息

print(“Amount details of the fraudulent transaction”)

fraud.Amount.describe()

输出 :

Amount details of the fraudulent transaction

count 492.000000

mean 122.211321

std 256.683288

min 0.000000

25% 1.000000

50% 9.250000

75% 105.890000

max 2125.870000

Name: Amount, dtype: float64

代码:打印正常交易的金额详细信息

print(“details of valid transaction”)

valid.Amount.describe()

输出 :

Amount details of valid transaction

count 284315.000000

mean 88.291022

std 250.105092

min 0.000000

25% 5.650000

50% 22.000000

75% 77.050000

max 25691.160000

Name: Amount, dtype: float64

从中我们可以清楚地注意到,欺诈者的平均货币交易更多。这使得这个问题变得至关重要。

代码:绘制相关矩阵

相关矩阵以图形方式让我们了解特征如何相互关联,并可以帮助我们预测与预测最相关的特征是什么。

# Correlation matrix

corrmat = data.corr()

fig = plt.figure(figsize = (12, 9))

sns.heatmap(corrmat, vmax = .8, square = True)

plt.show()

在 HeatMap 中,我们可以清楚地看到大多数特征与其他特征不相关,但有些特征彼此之间存在正相关或负相关。例如, V2和V5与称为Amount的特征高度负相关。我们还看到了与V20和Amount的一些相关性。这使我们对可用的数据有更深入的了解。

代码:分离 X 和 Y 值

将数据划分为输入参数和输出值格式

# dividing the X and the Y from the dataset

X = data.drop(['Class'], axis = 1)

Y = data["Class"]

print(X.shape)

print(Y.shape)

# getting just the values for the sake of processing

# (its a numpy array with no columns)

xData = X.values

yData = Y.values

输出 :

(284807, 30)

(284807, )

训练和测试数据分叉

我们将数据集分为两个主要组。一个用于训练模型,另一个用于测试我们训练好的模型的性能。

# Using Skicit-learn to split data into training and testing sets

from sklearn.model_selection import train_test_split

# Split the data into training and testing sets

xTrain, xTest, yTrain, yTest = train_test_split(

xData, yData, test_size = 0.2, random_state = 42)

代码:使用 skicit learn 构建随机森林模型

# Building the Random Forest Classifier (RANDOM FOREST)

from sklearn.ensemble import RandomForestClassifier

# random forest model creation

rfc = RandomForestClassifier()

rfc.fit(xTrain, yTrain)

# predictions

yPred = rfc.predict(xTest)

代码:构建各种评估参数

# Evaluating the classifier

# printing every score of the classifier

# scoring in anything

from sklearn.metrics import classification_report, accuracy_score

from sklearn.metrics import precision_score, recall_score

from sklearn.metrics import f1_score, matthews_corrcoef

from sklearn.metrics import confusion_matrix

n_outliers = len(fraud)

n_errors = (yPred != yTest).sum()

print("The model used is Random Forest classifier")

acc = accuracy_score(yTest, yPred)

print("The accuracy is {}".format(acc))

prec = precision_score(yTest, yPred)

print("The precision is {}".format(prec))

rec = recall_score(yTest, yPred)

print("The recall is {}".format(rec))

f1 = f1_score(yTest, yPred)

print("The F1-Score is {}".format(f1))

MCC = matthews_corrcoef(yTest, yPred)

print("The Matthews correlation coefficient is{}".format(MCC))

输出 :

The model used is Random Forest classifier

The accuracy is 0.9995611109160493

The precision is 0.9866666666666667

The recall is 0.7551020408163265

The F1-Score is 0.8554913294797689

The Matthews correlation coefficient is0.8629589216367891

代码:可视化混淆矩阵

# printing the confusion matrix

LABELS = ['Normal', 'Fraud']

conf_matrix = confusion_matrix(yTest, yPred)

plt.figure(figsize =(12, 12))

sns.heatmap(conf_matrix, xticklabels = LABELS,

yticklabels = LABELS, annot = True, fmt ="d");

plt.title("Confusion matrix")

plt.ylabel('True class')

plt.xlabel('Predicted class')

plt.show()

输出 :

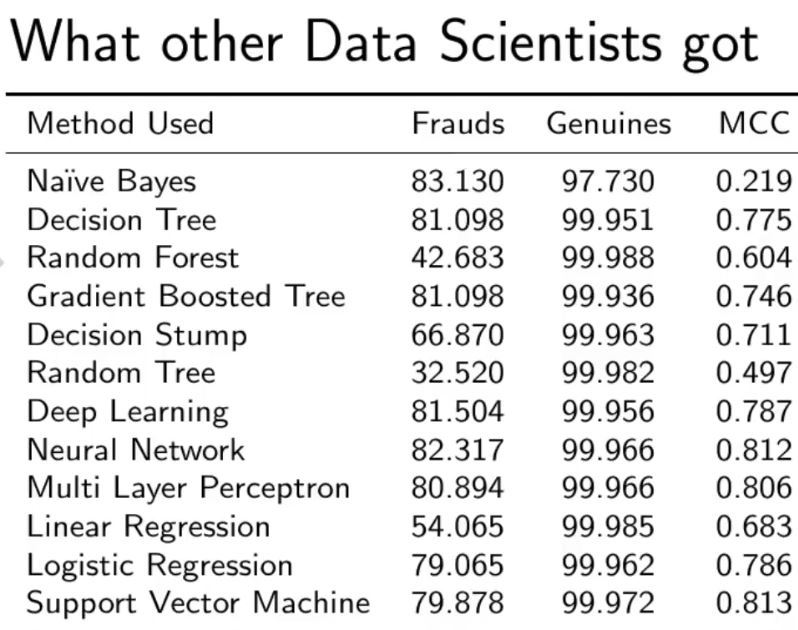

在不处理数据不平衡的情况下与其他算法进行比较。

正如您在我们的随机森林模型中看到的那样,即使对于最棘手的部分召回,我们也得到了更好的结果。

在评论中写代码?请使用 ide.geeksforgeeks.org,生成链接并在此处分享链接。